Bob Henderson found that there is nothing like losing $200 million during the 2008 financial crisis to concentrate the mind.

[T]he Federal Reserve… has conducted stress tests on the biggest banks every year since the crisis [of 2008]. The Fed’s goal is the same as mine was in September 2008: to calculate how bad things might get. In the Fed’s case, that means testing what might happen to the banks’ capital (assets minus debts) in a crisis when assets depreciate. Negative capital is called insolvency. For a bank, insolvency is a fast track to bankruptcy. In “supervisory†stress testing, regulators like the Fed—this is being done in Europe too—posit one or more worst-case scenarios and compute the consequences for capital, similar to how I tried to calculate how much I’d lose in a crash.

The Fed’s first test in 2009 was an unmitigated success, widely credited with ending the most acute stage of the crisis. The test was based on a scenario in which the market tanked even further than it already had and a deep recession followed. The Fed concluded that several big banks would suffer capital shortfalls as a result, Bank of America leading the list with a deficit of $33 billion. The Treasury Department then topped off the needy banks with cash from its Troubled Asset Relief Program, reassuring markets and kick-starting a recovery.

Now, the Fed stress tests the big banks every year, partly because the chief piece of post-crisis financial regulation in the U.S., the 2010 Dodd-Frank Act, requires it. Banks have long operated under regulatory capital limits, such as minimum ratios of capital to assets. What’s new since the crisis is that those minima have increased and that stress testing is used to regulate banks’ capital plans—limiting share buybacks and dividend payments, for example—to try to guarantee that they’ll have sufficient capital no matter what.

The Fed’s test in 2015 concluded that the 31 largest bank holding companies in the U.S., which account for more than 80 percent of the country’s banking assets, would lose a grand total of $490 billion in its worst-case scenario. And yet, for the first time in the tests’ history, not a single bank failed the test by having its capital to asset ratio fall below the Fed’s 5 percent hurdle. The implication was that the banks were finally under control.

Or was it just an illusion of control?

I took a look at the Fed’s stress test scenario1 myself recently, on the bank’s website. My first reaction was that it seemed almost farcically fashioned to “fight the last warâ€: The Dow drops by about half, U.S. GDP dips around 5 percent, unemployment spikes to 10 percent—basically it’s the aftermath of 2008 all over again. It doesn’t account for other potential calamities, like a breakup of the Euro, for example, or an emerging market crisis, or hyperinflation, or shock-induced feedback effects like the ones I faced with fuel.

There’s also the inconvenient fact that both Fannie Mae and Freddie Mac were stress tested regularly by their regulator, and declared well capitalized—right up until they failed in 2008. The same was true for Iceland’s banks.

I’m not alone in my skepticism. The former Fed economist Til Schuermann, who had a hand in designing the Fed’s tests, thinks that they actually add risk to the system, rather than reduce it, a position he outlined in a 2013 Wall Street Journal op-ed. “The danger is that the financial system and its regulators are moving to a narrow risk-model gene pool that is highly vulnerable to the next financial virus,†he wrote. “By discouraging innovation in risk models, we risk sowing the seeds of our next systemic crisis.â€

In other words, the Fed, by centralizing stress testing around its own approach, is incentivizing banks to follow suit, which may push them to accumulate similar exposures to one another and to manage them in similar ways, resulting in decreased diversification and increased risk. This is a question raised by particularly prescriptive rules like the Fed’s 5 percent hurdle, which are simple to monitor but may be just as simple to game.

What’s more, the Fed’s own incentives may support an illusion of control.

“They’re grading their own papers and they always pass,†said Kevin Dowd recently on a Cato Institute podcast. Dowd, another Fed stress test skeptic, is a professor of finance and economics at Durham University in England. “A central bank stress test can never be credible because of the incentives built in to get a pass result,†he added.

Dowd reasons that, given the Fed’s mandate to keep the financial system safe, it’s motivated to find that it is safe, similar to the way that I was incentivized to get stress testing results that supported doing my potentially mega-profitable deal.

You don’t argue when someone’s handing you a big check, but I wondered what the hell he was thinking.

I got Dowd on the phone recently and asked him what the Fed could do to improve its tests.

“First off, don’t do them,†was his response. So what model should the Fed use instead?

“I would not use any model at all. I do not believe financial risk modeling works,†he replied.

“It takes a model to beat a model,†I challenged, plagiarizing a phrase I’d learned from another professor of finance when I started in banking and which became something of a mantra of mine thereafter.

Dowd chuckled, but was unmoved. “I would always go for history over a model,†he replied, before explaining that he’d look to what capital levels were in the 19th century, when banks were private companies and less subject to government regulation.

J.D. Vance, the recent ex-Marine graduate of Yale Law School whose new book, Hillbilly Elegy, was discussed here not long ago, understands the social and economic pain that is causing his hometown friends and neighbors to look for quick relief, but he also recognizes that Trumpism is really the political equivalent of meth or heroin.

During this election season, it appears that many Americans have reached for a new pain reliever. It too, promises a quick escape from life’s cares, an easy solution to the mounting social problems of U.S. communities and culture. It demands nothing and requires little more than a modest presence and maybe a few enablers. It enters minds, not through lungs or veins, but through eyes and ears, and its name is Donald Trump.

Last Sunday, the day before Memorial Day, I met a Marine veteran of the Vietnam War at a local coffee shop. “I was lucky,†he told me. “At least I came home. A lot of my buddies didn’t. The thing is, the media still talks about us like we lost that war! I like to think my dead friends accomplished something.†Imagine, for that man, the vengeful joy of a Trump rally. That brief feeling of power, of defiance, of sending a message to the very political and media establishment that, for 45 years, has refused to listen. Trump brings power to those who hate their lack of it, and his message is tonic to communities that have felt nothing but decline for decades.

In some ways, Trump’s large, national coalition defies easy characterization. He draws from a broad base of good people: kind folks who open their homes and hearts to people of all colors and creeds, married couples with happy homes and families who live nearby, public servants who put their lives on the line to fight fires in their communities. Not all Trump voters spend their days searching for an analgesic.

Yet a common thread among Trump’s faithful, even among those whose individual circumstances remain unspoiled, is that they hail from broken communities. These are places where good jobs are impossible to come by. Where people have lost their faith and abandoned the churches of their parents and grandparents. Where the death rates of poor white people go up even as the death rates of all other groups go down. Where too many young people spend their days stoned instead of working and learning.

Many years ago, our neighbor (and my grandma’s old friend) in Middletown moved out and rented his house on a Section 8 voucher—a federal program that offers housing subsidies to low-income people. One of the first folks to move in called her landlord to report a leaky roof. By the time the landlord arrived, he discovered the woman naked on her couch. After calling him, she had started the water for a bath, gotten high, and passed out. Forget about the original leak, now much of the upstairs—including her and her children’s possessions—was completely destroyed. Not every Trump voter lives like this woman, but nearly every Trump voter knows someone who does.

Though the details differ, men and women like my neighbor represent, in the aggregate, a social crisis of historic proportions. There is no group of people hurtling more quickly to social decay. No group of people fears the future more, dies with such frequency from heroin, and exposes its children to such significant domestic chaos. Not long ago, a teacher who works with at-risk youth in my hometown told me, “We’re expected to be shepherds to these children, but they’re all raised by wolves.†And those wolves are here—not coming in from Mexico, not prowling the halls of power in Washington or Wall Street—but here in ordinary American communities and families and homes.

What Trump offers is an easy escape from the pain. To every complex problem, he promises a simple solution. He can bring jobs back simply by punishing offshoring companies into submission. As he told a New Hampshire crowd—folks all too familiar with the opioid scourge—he can cure the addiction epidemic by building a Mexican wall and keeping the cartels out. He will spare the United States from humiliation and military defeat with indiscriminate bombing. It doesn’t matter that no credible military leader has endorsed his plan. He never offers details for how these plans will work, because he can’t. Trump’s promises are the needle in America’s collective vein.

The great tragedy is that many of the problems Trump identifies are real, and so many of the hurts he exploits demand serious thought and measured action—from governments, yes, but also from community leaders and individuals. Yet so long as people rely on that quick high, so long as wolves point their fingers at everyone but themselves, the nation delays a necessary reckoning. There is no self-reflection in the midst of a false euphoria. Trump is cultural heroin. He makes some feel better for a bit. But he cannot fix what ails them, and one day they’ll realize it.

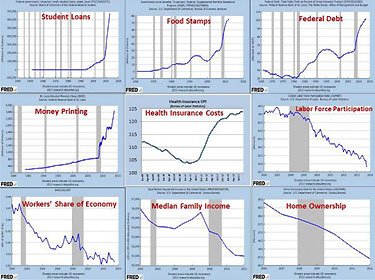

George Gilder explains that the ability of Wall Street to get rich while Middle Class America sinks deeper into unending recession doesn’t really have anything to do with Hispanic immigrants or Free Trade. The real cause is the nationalization of capital. These days Washington picks all the winners, and if you aren’t Goldman Sachs or the like, you haven’t got the necessary blat to be receiving any favors.

Why does Wall Street keep recovering after recessions but the economy seemingly never does?

The reason, as I document in my book, “The Scandal of Money: Why Wall Street Recovers but the Economy Never Does” is that Washington and the Federal Reserve together have created a closed loop economy where the Fed creates money for the government and the S&P 500 and Main Street is left out.

The Fed decides what money is worth and who receives it and how much. The Fed prices it at zero interest rates, allegedly to stimulate economic growth. But whenever something is free, it’s distributed by queue, and only the privileged, connected people in the front of the line get any, not the innovators who create growth and opportunity for Main Street. Trump voters are wrong if they blame Mexico and China, but they are right about one big thing: The economy is rigged against them.

The Fed takeover of the economy has turned Main Street into Mean Street; it has gelded Silicon Valley, reducing our most creative entrepreneurs to climate cranks obsequiously petitioning in Washington.

Almost two-thirds of jobs created between 2002 and 2010 came from 23 million small businesses, according to the Small Business Administration. But venture capital investment in 2014 of $48 billion is just one-third of the 2000 total (in 2015 dollars), according to the National Venture Capital Association. There were half as many IPOs in 2015 as in 2000, and they were mostly focused on a few large deals. Back in 1999, there were seven times more IPOs than mergers and acquisitions for tech companies. Today merger and acquisitions outnumber IPOs by almost 36 to 1.

The Fed regulations and money manipulations have displaced an open market of IPOs by an exclusive game of horse trading among “qualified investors” who get rich and leave Main Street out, and fail to create new jobs.

And Wall Street? The once powerful engine of capitalism has been nationalized by the Obama bureaucracies feeding on fines and fees. We’ve had a covert socialist coup in Washington and it must be reversed or the free enterprise engine of growth and opportunity is in jeopardy.

Rod Dreher understands, and sympathizes, with the anger that is causing a lot of people to rebel against the Establishment and support Donald Trump. He’s just sad at recognizing that Trump is a phony and that rebellion is going nowhere.

I’ve been pretty explicit in this space for some time about how I think the Donald J. Trump phenomenon is based in something real. I mean, the grievances to which he speaks are not phantoms. What I find impossible to accept is that Trump is anything other than a voice of resentment. If he offered some kind of way to redress those grievances, to do something concrete about them, things would be different. If he had the moral probity and personal character to lead others to solutions, things would be different. I keep wanting to think he does, and have been trying to give him the benefit of my own severe doubts about him. But after last night’s deplorable show on state in Detroit, it could not possibly be clearer that Trump will deliver for nobody. If he wins the presidency, he is going to betray the people who believe in him. That’s who he is. …

My own “burn baby burn†moment regarding the GOP was learning last fall from Congressional insiders that the party’s leadership had no plans for religious liberty legislation post-Obergefell. They don’t want to have to be told by the media that they’re all bigots. And, plainly, their deep-pocketed donors are embarrassed by the church people who give the Republicans their votes. So, screw us, is the thought.

I understand that Republicans cannot achieve, post-Obergefell, what people like me would like to see them achieve in terms of protecting traditional marriage. That ship has sailed. The culture has shifted. It’s unreasonable to expect the moon.

But for pity’s sake, when the Republican Party cannot bring itself to defend religious liberty, and the right of church people who don’t sell their Christianity out to be left alone, what bloody use are they? …

We are …watching the ongoing dispossession of people in this country of their history, at the hands of progressives — and the forces of political conservatism are saying nothing about it. From the front page of the Stanford University newspaper yesterday, a report about a move underway to purge the campus of all references to St. Junipero Serra, a Catholic missionary who was a pivotal figure in California history. Excerpt:

Leo Bird ’17 introduced the resolution in the ASSU senate. Bird, who prefers to be referred to by the gender neutral “they,†said that they were motivated by what they saw as the discrepancy between Serra’s actions toward Native Californians and his legacy on Stanford’s campus.

“It really started out of conversations that I started to have my freshman year at the Native American cultural center,†Bird explained. “I started to get involved with Bay Area activism and started to recognize that there was this historical figure [Serra] that was represented that was sort of praised, honored, in a way that I felt really did a disservice to a lot of the California Native community as well as to my own identity, being here at Stanford.â€

“They.†Good lord. This is the kind of person who triumphs, over and over, because our universities and the elites they serve have gone corrupt and insane. Who stands up to this? They win and they win and they win. If people conclude that they are being dispossessed in their own country, and the Republican Party is effectively colluding with the dispossession, then who can be surprised by a backlash that takes the form of support for Trump? When the left wages culture war, as it constantly does, it should not be surprised that at least some conservatives see the only one on their side who brings any kind of fight to the battle is an extreme vulgarian named Donald Trump.

I’m not defending Trump. I’m trying to explain his appeal. Believe me, my heart wants the Republicans to be spatchcocked and grilled, but my head says that the country would take an unacceptable risk with Trump in the White House.

Scott Grannis calculates just how much economic growth we’ve lost, for some unknown reason, over the course of the last six years.

Real GDP growth in the first quarter was weaker than expected (0.2% vs. 1.0%), but it wasn’t much of a surprise. It’s now been almost six years that the economy has managed only meager growth—about 2 ¼% per year on average. As a result, by my calculations, real GDP is a little over 10% below its long-term trend potential. That’s more than $2 trillion in lost income every year, and it’s getting worse. …

The chart above compares the level of real GDP to a long-term trend growth rate of 3.1%. This confirms once again that we are stuck in the slowest recovery ever. It’s my belief that the persistence of slow growth is largely the result of bad policies, though demographics likely plays a part too. Corporate profits have been very strong, but business investment has been very weak. Without new investment and risk-taking, we are not going to see a pickup in productivity which is, at the end of the day, what drives stronger growth and higher living standards. Investment has been weak probably because marginal tax rates and regulatory burdens have increased significantly in the past six years. In a sense, and expansion of government has suffocated the private sector.

Things are not going to change much for the better until policies become more pro-growth.

Whether the persistence of relatively weak growth is a reason for the Fed to continue to keep short-term interest rates extraordinarily low is one of the key questions of our time. I don’t see how low interest rates stimulate investment or enhance productivity. Only private initiatives can do that.

On the bright side, if policies do become more favorable, there is tremendous upside potential to look forward to. Closing the GDP gap would be nothing short of exhilarating.

Douglas Holtz-Eakin attempts to calculate the impact of the 2010 Dodd–Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) on the growth of the economy.

What did Dodd-Frank do to the effective tax rate on banks? Consider, first, the burden of complying with the new regulations. The American Action Forum’s analysis of the Federal Register indicates that the cumulative burden (including the market value of paperwork hours for compliance) is roughly $14.8 billion annually. Notice that after-tax income in the presence of the burden is:

[rL – C – Burden](1-tB)

where r is interest on loans (L), C is the cost of acquiring funds and other operations, and tB is the tax rate on banks. Suppose that instead of a burden, the same after-tax income was generated by simply raising the tax rate to t’. Then, by definition:

[rL – C – Burden](1-tB) = [rL – C](1-t’)

[which] can be re-arranged to yield:

t’ = tB + (1-tB)[Burden/(rL-C)]

To put some empirical meat on [this], the Federal Deposit Insurance Corporation’s (FDIC) Quarterly Banking Profile (QBP) provides information on taxes ($67.5 billion) and net income ($151.2 billion) that permit one to compute an initial tax rate of 31 percent. Using the AAF burden data and (11) yields an increase to 37.8 percent from compliance burdens.

A similar approach can be used to transform the roughly 2 percentage point rise in the leverage ratio of the banking sector (from 7.5 to 9.5 percent) from 2008 to 2014 into a rise in the effective tax rate. The banking sector responded to Dodd-Frank by holding more equity capital, thus require it to have greater earnings to meet the market rate of return – the same impact as raising taxes. In this case, the higher leverage ratio translates into a further increase in the effective tax rate to 40.3 percent, for a total rise of 9.2 percent.

Collecting results, the impact on economic growth is a decline in the per capital growth rate of 0.059 percentage points annually. Is this a big deal? Consider lowering the growth rate in the Congressional Budget Office baseline projections by exactly this amount between 2016 and 2025. The lower rate of economic growth translates into a total loss of $895 billion in GDP or $3,346 for every member of the working age (16 and older) population over those 10 years.

Kurt Schlichter enjoys a good laugh at the Dummer Junger‘s expense.

There’s no sugar-coating it – your votes for Democrats have ensured that you are the first generation in American history that will fail to exceed what their parents attained. Embracing liberalism was a stupid thing to do, done for the stupidest of reasons, and I will now let you subsidize my affluent lifestyle without a shred of guilt.

I’m a 48 year old trial lawyer living on the coast in California – I should have “Hope and Change†tattooed on my glutes. I’d have an excuse to be lib-curious, but you Millennials? Why do you support an ideology that pillages you to pay-off Democrat constituencies? Your time in the indoctrination factories of academia trained you in a form of “critical thinking†that is neither. Somehow, you came to embrace the bizarre notion that conservatives are psychotic Jesus freaks who want to Footloosisze America into a land of mandatory Sunday school and no dancing.

But liberals, in contrast, are nice. Obama is cool. You chose petty fascism with a smile. Not a lot of thought went into it. Facts, evidence – these were mere distractions from the feelings-based validation that came from rejecting us wicked conservatives.

What did you get? The chance to be forced to buy health insurance you don’t want at inflated rates so my rates can be lower. You get to pay more out of your monthly barista take – liberalism ensured that the tanked job market foreclosed a real career – so that I get to pay less out of my lawyer checks. Thanks, suckers.

You fume that conservatives want to spy on you in your bedrooms. Leaving aside the fact that that your tacky boudoir fumblings are the last thing conservatives care about, have you noticed how your precious Big Brother spies on your doings everywhere else? But who cares about that – Mumford & Sons totally digs Obama!

Don’t even get me started on your crappy music.

Enjoy your student loans, Millennials! We tried to tell you that it was a Democrat scam designed to subsidize liberal academia by allowing you to go into decades of crushing debt to pay for a bachelors in Ancient Guatemalan Gender Identity Issues.

Good plan. Now fetch my latte – I’m in a hurry to get to my corner office. And I’ll leave you a tip – next time you decide to vote for a liberal, first be born in 1964.

Don’t think that I’m happy about this. I came to Los Angeles after the Gulf War. I had a car and a few bucks I had saved in the desert which went right into paying for Loyola Law School. I had no contacts and no money, but I knew I had endless opportunity.

I worked hard. I could start a business. I could get credit. I could – and did – build my own future.

But can you? Liberalism, with its impoverishing redistribution, crippling regulations and the debt it suckered you into undertaking, has ensured that most of you can’t.

You live with your parents, and Obamacare encourages sponging until you are 26 years old. At 26, I was leading Americans in a war, not begging mommy to pay my bills. The liberals want you to be eternal man-children, wearing cargo shorts and passively pumping money into their socialized medicine nightmare in return for “Brosurance†you don’t want or need.

So feel free to keep voting for the liberals who keep you in chains. I’ll take my cheaper insurance, my future Social Security checks, and the other benefits that come from being established without guilt. The guys who you squander your votes upon certainly won’t change that equation. You’ll tread water in life, but hey, at least those conservatives won’t be in charge!

On the eve of Obamacare’s arrival, Mark Steyn assesses what the age of Obama has accomplished for Americans.

President Obama has added six-and-a-half trillion bucks to the national debt, and has nothing to show for it. As Churchill would say, had his bust not been bounced from the Oval Office, never in the field of human spending has so much been owed by so many for so little. …

My colleague Michelle Malkin revealed this week that her family has now joined the massed ranks of Obamacare victims: Anthem BlueCross BlueShield sent her a “Dear John†letter, explaining why they’d be seeing less of each other. “To meet the requirements of the new laws, your current plan can no longer be continued beyond your 2014 renewal date.â€

Beyond the president’s characteristically breezy lie that “if you like your health care plan, you will be able to keep your health care plan†is the sheer nuttiness of what’s happening. For years, Europeans and “progressive†Americans have raged at the immorality of the U.S. medical system: All those millions with no health coverage! But Michelle Malkin had coverage and suddenly, under what Obama calls “universal health care,†she doesn’t. The CBO’s most recent calculations estimate that, in 2023, a decade after the implementation of Obamacare, there still will be more than 30 million people uninsured – or about the population of Canada. That doesn’t sound terribly “universal,†and I would bet it’s something of a low-ball figure: As many employers are discovering, one of the simplest ways “to meet the requirements of the new laws†and still stay just about solvent is to shift your workers from family plans to individual plans, and tell their spouses and children to go look elsewhere. Does it achieve its other goal of “containing costs,†already higher than anywhere else? No. Avik Roy reports in Forbes that Obamacare will increase individual-market premiums by 62 percent for women, 99 percent for men. In America, “insuring†against disaster now costs more than you’d pay in most countries for disaster.

No one has ever before attempted to devise a uniform health system for 300 million people – for the very good reason that it probably can’t be done. Britain’s National Health Service serves a population less than a fifth the size of America’s and is the third-largest employer on the planet, after the Indian National Railways and the Chinese People’s Liberation Army, the last of which is now largely funded by American taxpayers through interest payment on federal debt. A single-payer U.S. system would be bigger than Britain’s NHS, India’s railways and China’s army combined, at least in its bureaucracy. So, as in banking and housing and college tuition and so many other areas of endeavor, Washington is engaging in a kind of under-the-counter nationalization, in which the husk of a nominally private industry is conscripted to enforce government rules – and ruthlessly so, as Michelle Malkin and many others have discovered.

Obama’s pointless, traceless super-spending is now (as they used to say after 9/11) “the new normal.†Nancy Pelosi assured the nation last weekend that everything that can be cut has been cut and there are no more cuts to be made. And the disturbing thing is that, as a matter of practical politics, she may well be right. Many people still take my correspondent’s view: If you have old money well-managed, you can afford to be stupid – or afford the government’s stupidity on your behalf. If you’re a social-activist celebrity getting $20 million per movie, you can afford the government’s stupidity. If you’re a tenured professor or a unionized bureaucrat whose benefits were chiseled in stone two generations ago, you can afford it. If you’ve got a wind farm, and you’re living large on government “green energy†investments, you can afford it. If you’ve got the contract for signing up Obamacare recipients, you can afford it.

But, out there, beyond the islands of privilege, most Americans don’t have the same comfortably padded margin for error, and they’re hunkering down. Obamacare is something new in American life: the creation of a massive bureaucracy charged with downsizing you – to a world of fewer doctors, higher premiums, lousier care, more debt, fewer jobs, smaller houses, smaller cars, smaller, fewer, less; a world where worse is the new normal. Would Americans, hitherto the most buoyant and expansive of people, really consent to live such shrunken lives? If so, mid-20th century America and its assumptions of generational progress will be as lost to us as the Great Ziggurat of Ur was to 19th century Mesopotamian date farmers.

George Orwell, after attending a meeting of impoverished but passive miners, remarked sadly that “there is no turbulence left in England.†The Democrats, and much of the Republican establishment, have made a bet that there is no turbulence left in America, and the citizenry will stand mute before Obamacare’s wrecking ball. Unless they’re willing to accept a worse life for their children and grandchildren, middle-class Americans need to prove them wrong.