Rembrandt, Belshazzar’s Feast, 1635, National Gallery, London

Mark Steyn, in his customarily brilliant manner, reflects on the scope and significance of the federal debt.

The fecklessness of Washington is an existential threat not only to the solvency of the republic but to the entire global order. If Ireland goes under, it’s lights out on Galway Bay. When America goes under, it drags the rest of the developed world down with it. When I go around the country saying stuff like this, a lot of folks agree. Somewhere or other, they’ve a vague memory of having seen a newspaper story accompanied by a Congressional Budget Office graph with the line disappearing off the top of the page and running up the wall and into the rafters circa mid-century. So they usually say, “Well, fortunately I won’t live to see it.†And I always reply that, unless you’re a centenarian with priority boarding for the ObamaCare death panel, you will live to see it. Forget about mid-century. We’ve got until mid-decade to turn this thing around.

Otherwise, by 2020 just the interest payments on the debt will be larger than the U.S. military budget. That’s not paying down the debt, but merely staying current on the servicing — like when you get your MasterCard statement and you can’t afford to pay off any of what you borrowed but you can just about cover the monthly interest charge. Except in this case the interest charge for U.S. taxpayers will be greater than the military budgets of China, Britain, France, Russia, Japan, Germany, Saudi Arabia, India, Italy, South Korea, Brazil, Canada, Australia, Spain, Turkey, and Israel combined.

When interest payments consume about 20 percent of federal revenues, that means a fifth of your taxes are entirely wasted. Pious celebrities often simper that they’d be willing to pay more in taxes for better government services. But a fifth of what you pay won’t be going to government services at all, unless by “government services†you mean the People’s Liberation Army of China, which will be entirely funded by U.S. taxpayers by about 2015. When the Visigoths laid siege to Rome in 408, the imperial Senate hastily bought off the barbarian king Alaric with 5,000 pounds of gold and 30,000 pounds of silver. But they didn’t budget for Roman taxpayers picking up the tab for the entire Visigoth military as a permanent feature of life.

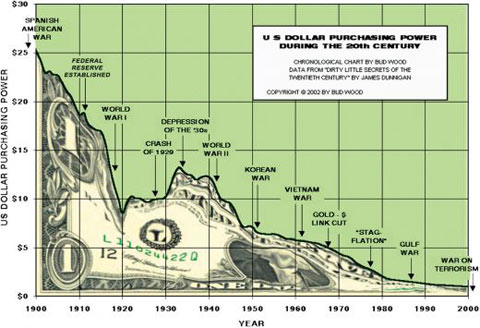

I think myself that Mark is overlooking the obvious detail: that when, as he puts it, “you get your MasterCard statement and you can’t afford to pay off any of what you borrowed but you can just about cover the monthly interest charge,” before much longer you wind up stiffing all your credit cards and burning your credit rating for the next decade. The government equivalent of stiffing credit cards consists of inflating your currency, so you can pay your debts after all using funny money worth a small fraction of what it was at the time those debts were incurred.

The US Government has not overlooked this solution. Remember Quantitative Easing? It is already underway and in process. I’m not sure who it was that remarked “Inflation is the cruelest tax,” but he was clearly right. Inflation rewards the improvident and punishes the responsible. Inflation strips the middle class of its accumulated savings in order to relieve the government of its debt.

Joe Queenan does a fine job of mocking the federal government’s “core inflation rate” calculation methodology.

[I]magine my surprise when the latest economic data came out and we were told that inflation wasn’t much of a problem at all. The price index for core personal consumption expenditures increased a piddling 0.9% from the previous year, keeping the national inflation rate far, far below what economists see as the danger level.

Hang on a second, I thought: What about my exorbitant fuel costs and the two bucks for my disgusting coffee and the $1.25 for my stale, tasteless bagel, with no schmear, no butter, no nothing? If inflation had jumped just a puny 0.9% in the past 12 months, why did it feel like everything that I bought last week had gone up 25%?

The answer lies in the way economists calculate what they call “core” price indexes. The core personal consumption expenditures index (PCE), for example, computes the cost of a representative basket of goods that consumers might buy—like used copies of “Madden 2009” and lace camisoles and jumbo-size containers of Percocet and personally autographed Kenny Chesney guitar picks and Blu-ray discs of “AVP: Alien vs. Predator” —but it cuts out variables like food and energy prices. This makes the month-to-month reporting on inflation less volatile, far less subject to the vicissitudes of the market.

At first glance, this seems baffling. Removing fuel and food costs from the index purely for the sake of statistical balance seems a bit like saying, “All told, four million people died in World War II. Well, unless you include the people who died in concentration camps. And, oh yeah, the 20 million Russians.” It’s a bit like saying, “On average, a major league baseball team will win 3.2 World Series each century. Obviously, not the Cubs. And we’ve thrown out the New York Yankees and their 27 world championships because it doesn’t provide a true snapshot of the game at any given moment.” It’s a bit like saying, “Billy Joel never wrote a single song that just totally sucks and makes people’s skin crawl. Unless you include ‘Captain Jack.’ Which we deliberately left out of our sample because it skews the results. Maybe we should have left out ‘Piano Man,’ too.”

French politician Rachida Dati says “fellatio” comment was slip of tongue.

Former French justice minister Rachida Dati has said the reason the word inflation came out as fellatio during her talk, was because she was speaking too fast.

Dati, 44, laughed at the mistake she had made on Canal Plus television during a radio interview.

“I just spoke too quickly but, well, if that lets everybody have a laugh, then that’s fine,” News.com.au quoted her as saying.

The MEP had confused oral sex with rising prices as she launched an attack on foreign investment funds.

“When I see some of them looking for returns of 20 or 25 percent, at a time when fellatio is close to zero, and in particular in a slump, that means we are destroying businesses,” she had told Canal Plus in a midday interview.

Warren Buffett spouts conventional pieties in the New York Times, but in the middle of Warren’s bromidal call for fiscal responsibility, the astute reader will find a shrewd assessment of what is really going to happen.

With government expenditures now running 185 percent of receipts, truly major changes in both taxes and outlays will be required. A revived economy can’t come close to bridging that sort of gap.

Legislators will correctly perceive that either raising taxes or cutting expenditures will threaten their re-election. To avoid this fate, they can opt for high rates of inflation, which never require a recorded vote and cannot be attributed to a specific action that any elected official takes. In fact, John Maynard Keynes long ago laid out a road map for political survival amid an economic disaster of just this sort: “By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens…. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.â€